Features:

- Calculates capital gains and estimates tax using FIFO and LIFO

- Long and short positions: stocks, ETFs, crypto-currencies,

- Detailed and configurable reports - you can filter the report by date or by product/equity name

- Export the reports to a spreadsheet for further custom analysis

- Supports CSV files or copy-pasted transaction data

- Flexible import formats - specify the file format and save it as a template

- Free, no subscription, no data harvesting, no advertising.

How it works?

Upload your data

Upload a file with your transaction data or simply copy-paste it.

Don’t worry about transaction format.

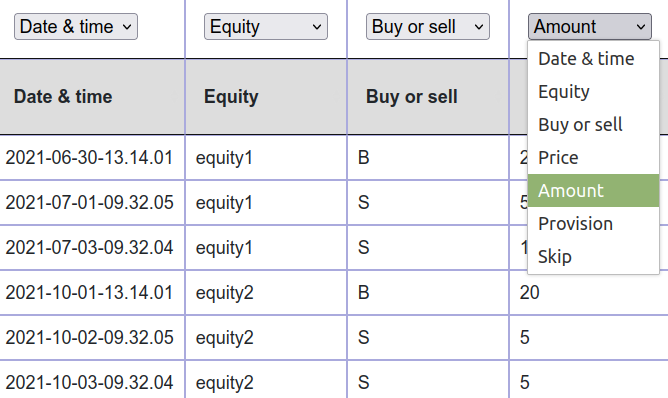

Describe the format

Interactively describe the format of your data.

Provide information using a simple interactive form.

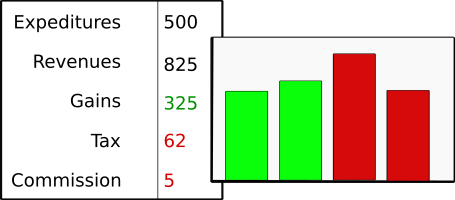

Analyze results

- Check out your capital gains, taxes, and commissions.

- Calculate the statistics for the whole portfolio and individual equities. Investigate every equity and every transaction in your portfolio